⚡ Transrail Lighting: The Backward-Integrated Play in a Growing T&D Market

The global Transmission & Distribution (T&D) market is booming, yet few players control the key margin levers. Transrail Lighting does. Over 90% of its business comes from T&D, and 65–70% of its contract value comes from products it manufactures in-house — towers, conductors, and monopoles.

With a footprint in 59 countries and four decades of experience, the company is now executing a ₹520 crore capex plan to more than double tower and conductor manufacturing capacity by mid-2026. This scale and backward integration give it both a cost edge and execution reliability, setting it apart from peers as domestic and international T&D projects surge.

Company Overview

Transrail Lighting is a global EPC powerhouse headquartered in India, with operations spanning 59 countries across five continents. With over 2,200 employees, the company delivers turnkey solutions across design, engineering, supply, manufacturing, construction, testing, and commissioning. Its six verticals — Power Transmission & Distribution, Substations, Civil Construction, Railways, Poles & Lighting, and Solar EPC — cover almost every critical aspect of energy and infrastructure projects.

In the Power T&D segment, which accounts for over 90% of revenues, Transrail has supplied 1.35 million MT of towers, executed lines up to 1,200kV, and completed substations in challenging terrains. Beyond India, it has executed landmark projects in Africa and Asia, positioning itself as a reliable partner for both government and multilateral-funded international projects.

Business Verticals

Power Transmission & Distribution

Power Transmission & Distribution remains the backbone of Transrail, contributing roughly 90–92% of total business. The company offers end-to-end EPC solutions, from line design and engineering to manufacturing, construction, testing, and commissioning. Its in-house manufacturing capabilities — towers, monopoles, and conductors — account for 65–70% of contract value, giving it significant control over the most critical and value-accretive components of its projects. Specialized EPC equipment, including stringing machines, cranes, launching gantries, and piling rigs, is supported by a central maintenance workshop in Butibori, Nagpur, ensuring minimal downtime and uninterrupted project execution.

Transrail is expanding beyond overhead lines into underground cabling for transmission and distribution networks and has a strong footprint in rural electrification, bringing reliable electricity to households across India and select international markets. Substation EPC is another major growth driver, with capabilities across high-voltage AIS, GIS, hybrid, renewable, mobile, and distribution substations, making it a one-stop solution for grid modernization.

Civil Construction and Railways

Civil Construction and Railways form selective, high-value verticals, with current bid pipelines of approximately ₹2,000 crore each, reflecting a focus on margin-accretive projects rather than volume chasing. Landmark civil projects include India’s longest river bridge over the Kosi (10 km) and the second tallest natural draft cooling tower in India (199 meters). In railways, Transrail has supplied metro and railway portals, overhead contact rods, and is executing electrification, signalling, and track linking projects, further strengthening its PQ credentials for future high-value orders.

Poles & Lighting

Poles & Lighting is another differentiator, primarily serving the Indian market with select international projects. Products have been deployed in flagship infrastructure projects like the Mumbai Trans Harbour Link, M. Chinnaswamy Stadium, and Samruddhi Highway, as well as internationally in Qatar’s stadium lighting and Zambia’s Lusaka city decongestion project. With 474,000 poles supplied and a newly expanded signage facility, Transrail is well-positioned to capture the growing demand for urban infrastructure, decorative lighting, and smart city initiatives.

Solar EPC

Solar EPC, a nascent but strategic focus, targets utility-scale projects overseas, with design, engineering, procurement, and construction capabilities up to 100 MWp for solar PV and 300 MWp for BoS/hybrid projects. Domestic bidding has not yet started, as the company spent the last year building the team, processes, and infrastructure, laying the groundwork for a future entry into India’s solar EPC market.

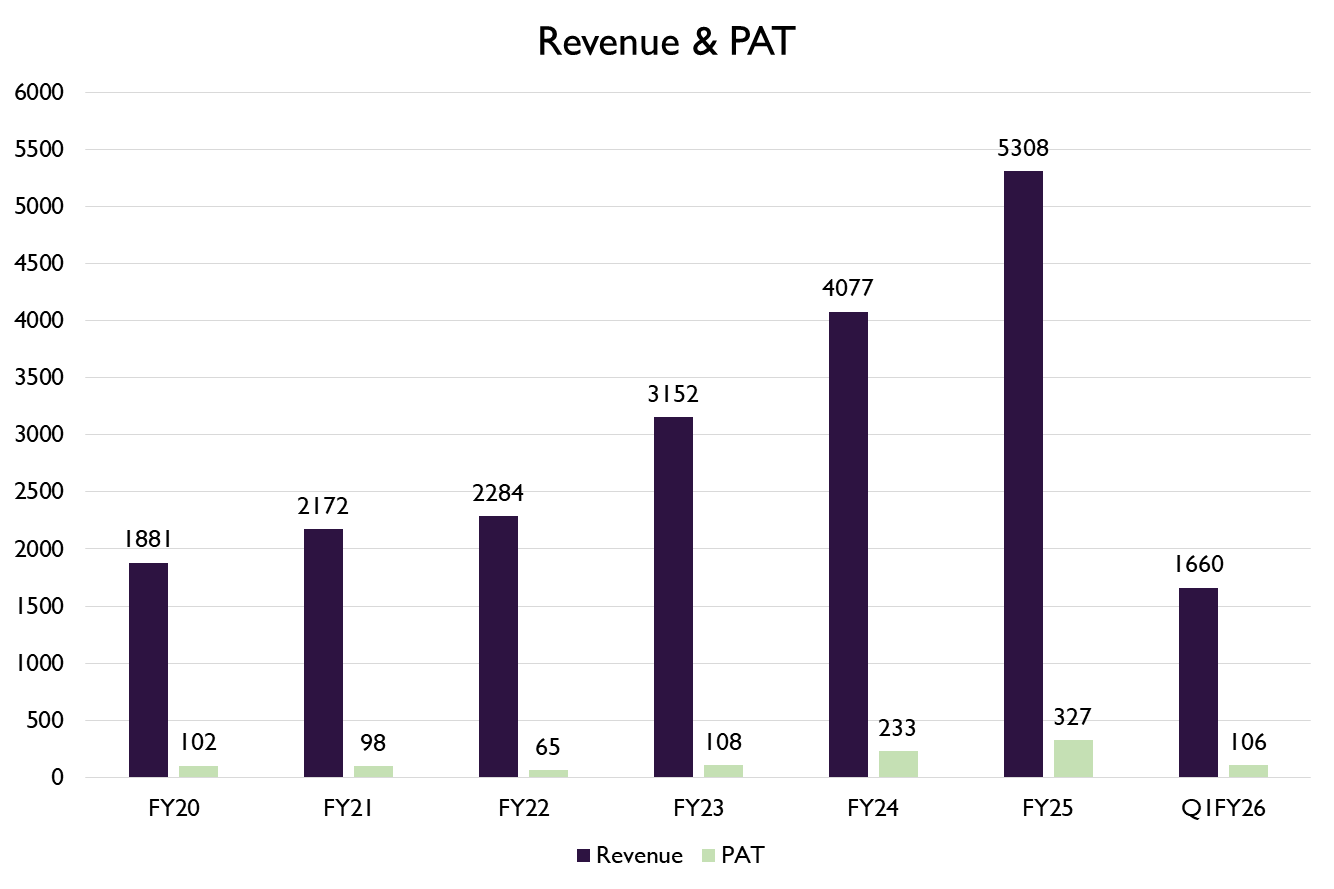

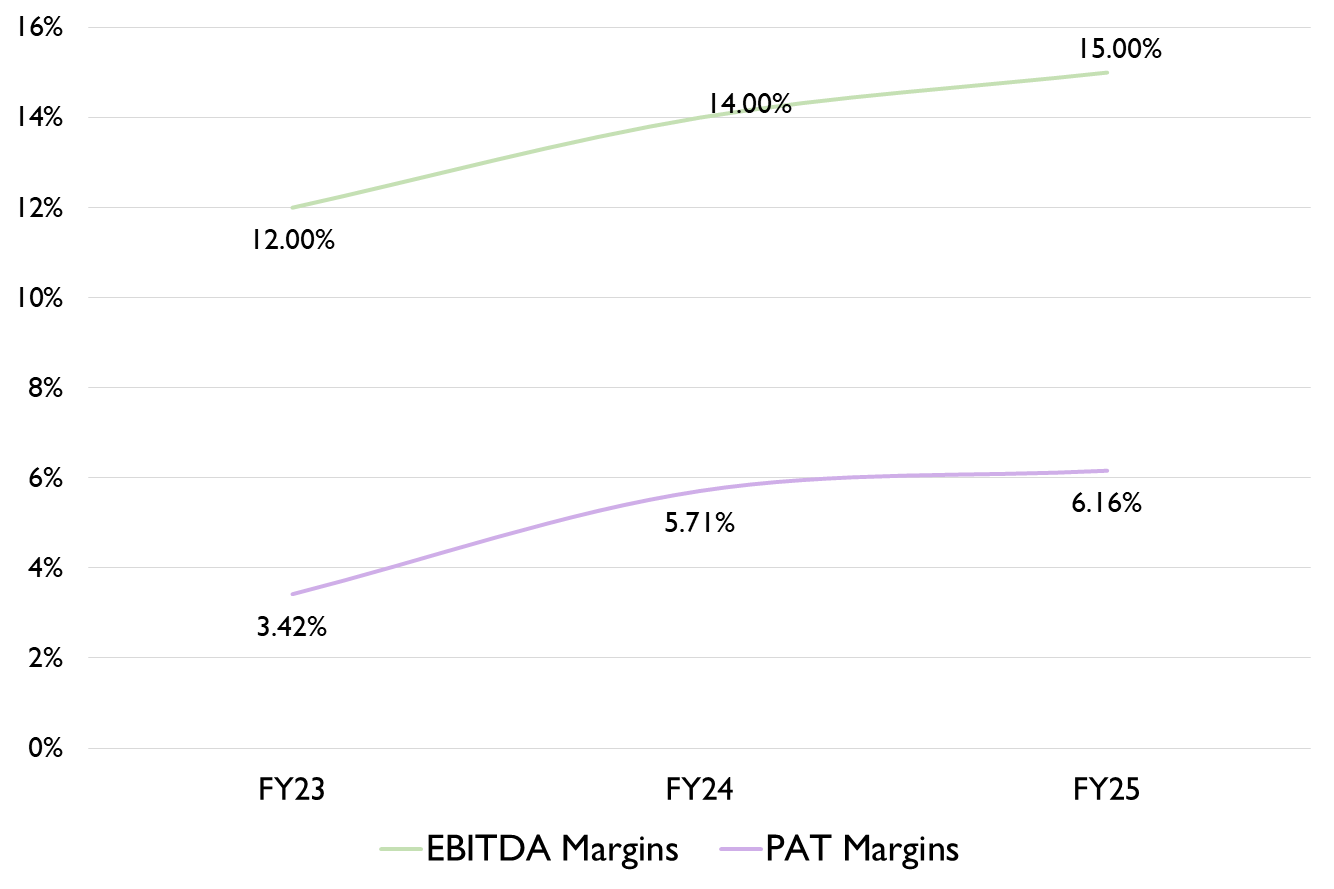

Financials

Manufacturing Footprint & Strategic Capex: Building Scale for Growth

Transrail’s competitive edge lies in its backward integration, allowing it to control the most critical and value-accretive components of its Transmission & Distribution projects, ensuring both execution reliability and margin protection.

Its manufacturing capabilities span towers, conductors, and poles, each designed to meet complex domestic and international project requirements:

Towers (Deoli & Vadodara): Produces the full range of transmission towers from 66kV to 800kV, including multi-circuit configurations for twin, quad, and hex conductors. Current capacity: 84,000 MT (95% utilisation).

Conductors (Silvassa): Manufactures conventional as well as High Temperature Low Sag (HTLS) and high-performance conductors, including AAAC, ACAR, AAC, ACSR, and ACSR/AW. Current capacity: 24,000 km (100% utilisation).

Poles (Silvassa): Designs, fabricates, and galvanises all types of pole structures for roads, railways, stadiums, urban infrastructure, and select international projects.

To support its growth trajectory and robust order book, Transrail is executing a ₹520 crore capex plan (FY26–27), structured as follows:

Funding mix: ₹90 crore from IPO proceeds, ₹300 crore sanctioned debt, remainder via internal accruals.

This capex will more than double tower and conductor capacity, underpinning execution of both domestic and international projects, maintaining healthy margins, and supporting selective expansion into new verticals such as solar EPC. The scale, integration, and operational control provided by this manufacturing footprint position Transrail to capitalize on the growing global T&D market while retaining its competitive edge.

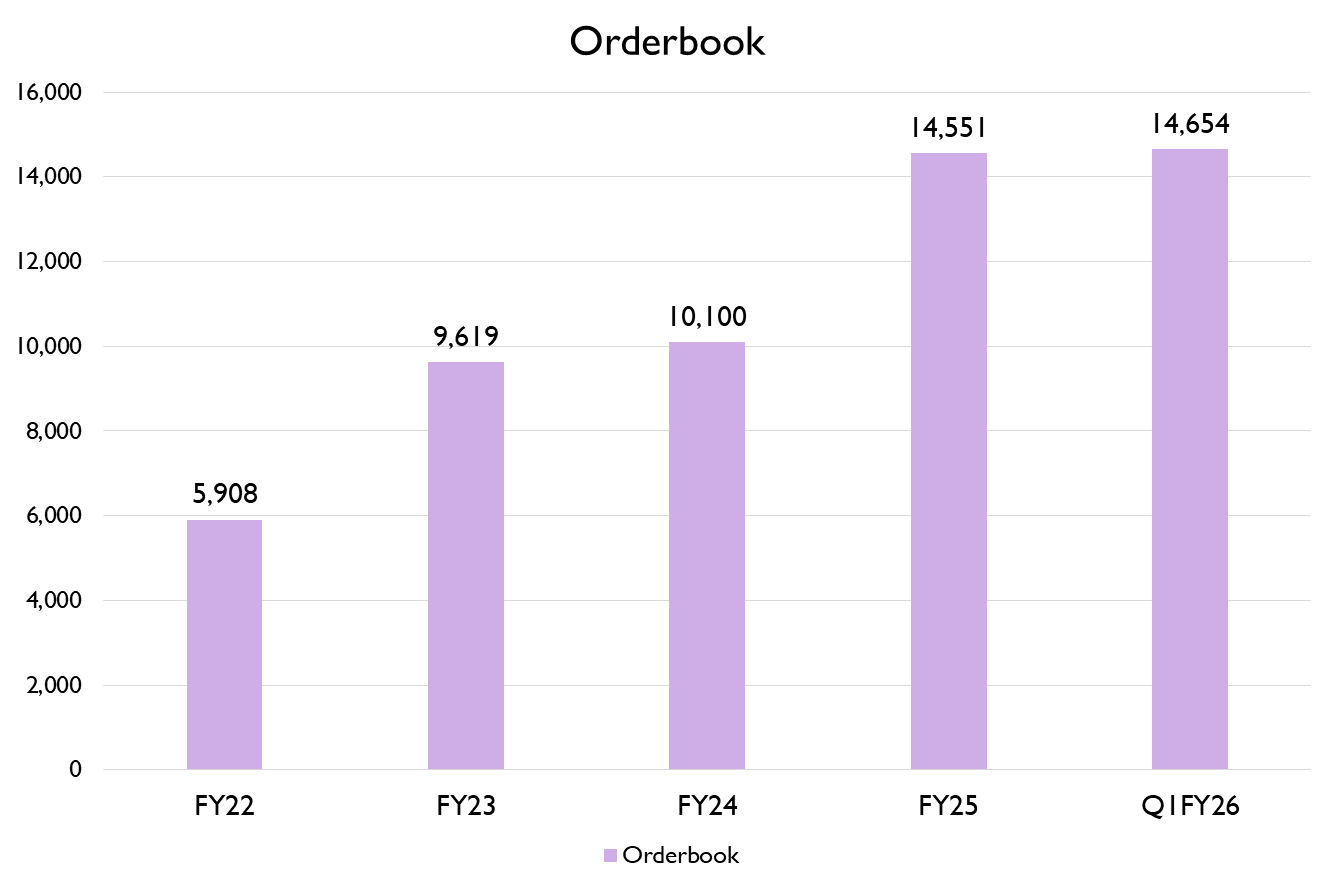

Order Book: Visibility & Execution

As of June 30, 2025, Transrail’s unexecuted order book including L1 stands at ₹15,637 crore, with 93% in T&D, split 60:40 between domestic and international. Average execution cycles are 18–24 months for domestic orders and 24–30 months for international projects, with only ~30% expected to execute in FY26.

Q1FY26 Highlights:

Order inflow: ₹1,748 crore (+72% YoY), including India’s domestic T&D lines and the largest substation project in Africa.

Execution completed: two 765kV lines, three 400kV lines, and one African project.

Pipeline & Strike Rate:

12-month market opportunity: ₹1,00,000 crore (50:50 domestic:international).

Planned bidding: ₹25,000 crore in the next 3–4 months, with 8–10% strike rate.

Domestic mix: 70–80% government, 20% private; international projects mainly funded by multilateral agencies.

With this pipeline and selective bidding strategy, management expects FY26 order inflows to match last year’s ₹9,500 crore, providing multi-year revenue visibility. Below table shows company’s orderbook over time.

Future Outlook: Selective, Margin-Accretive Growth

Focused Strategy: Transrail is focused on executing margin-accretive projects in Transmission & Distribution, while selectively expanding into civil, railways, poles & lighting, and overseas solar EPC. The company’s approach ensures growth without compromising profitability.

Growth & Margins: The company targets 22–25% revenue growth with EBITDA margins of 11.5–12%, leveraging its backward integration and operational control to maintain healthy project economics.

Capex & Expansion: Ongoing capex will scale tower and conductor capacity 2–2.5x, strengthen manufacturing capabilities, and open new markets through overseas solar EPC projects. This positions Transrail to execute its robust order book efficiently.

Financial Outlook: Debt is expected to rise to ₹800–900 crore by March 2026, partially mitigated by a potential CRISIL rating upgrade, which could reduce borrowing costs.

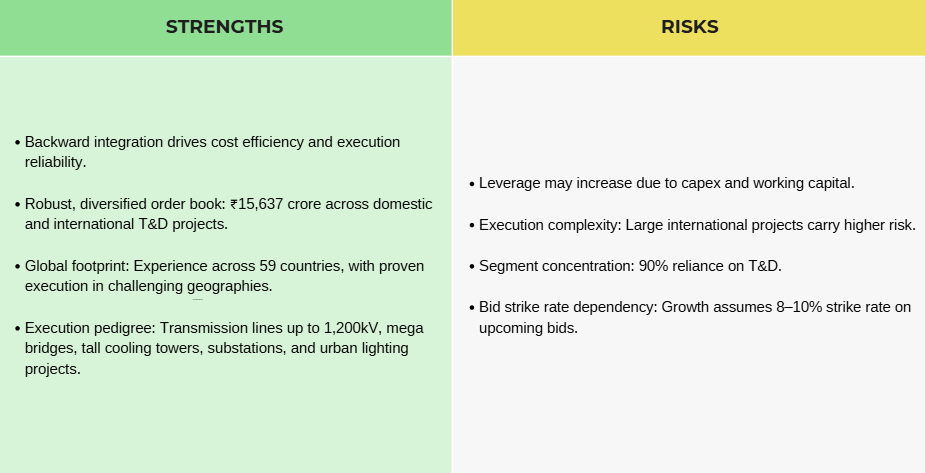

Strengths & Risks

If you an investor who keeps looking for such analysis on small & mid cap stocks, you can join our Emerging Titans model portfolio where we share detailed reports on such ideas. We are SEBI registered Research Analyst (with Registration No. INH000019789)

Disclosure

This article is for educational purposes only and does not constitute investment advice. Readers should consult a SEBI-registered advisor before making investment decisions.

Standard warning

“Investment in securities market are subject to market risks. Read all the related documents carefully before investing.“

Disclaimers

“Registration granted by SEBI, enlistment with RAASB and certification from NISM in no way guarantee performance of the Research Analyst or provide any assurance of returns to investors.”