Sundrop Brands Limited: Comprehensive Business Overview, Strengths, Risks, and Future Prospects

A candid analysis of Sundrop Brands’ diversified portfolio, recent strategic moves, operational challenges, and growth opportunities

Sundrop Brands Limited has rapidly evolved from its roots as Agro Tech Foods into a multifaceted food platform, combining iconic legacy brands with new growth avenues through strategic acquisitions. As it stands at a pivotal growth juncture, understanding the company’s true strengths and inherent risks becomes vital for stakeholders. This analysis offers an unvarnished view of how Sundrop is navigating competitive dynamics, operational integration, and market trends to build a sustainable and profitable food enterprise for the modern consume

Business Overview

Sundrop Brands Limited (formerly Agro Tech Foods) is a food company transitioning into a scaled food platform with multiple market-leading brands. It aims to deliver innovative, convenient, and delicious packaged food solutions to modern consumers, focusing on convenience foods, snacking, culinary products, and edible oils. The company leverages significant manufacturing, distribution, and marketing resources to grow in emerging and fast-growing channels such as e-commerce and modern retail.

The company operates nine manufacturing facilities across India and Bangladesh, reaching about 500,000 retail outlets with 1,800 distributors and 1,700 sales personnel. Its business model combines organic growth with inorganic expansion, notably through the acquisition of Del Monte Foods India business, which significantly broadened its product portfolio.

Business Segments and Revenue Splits

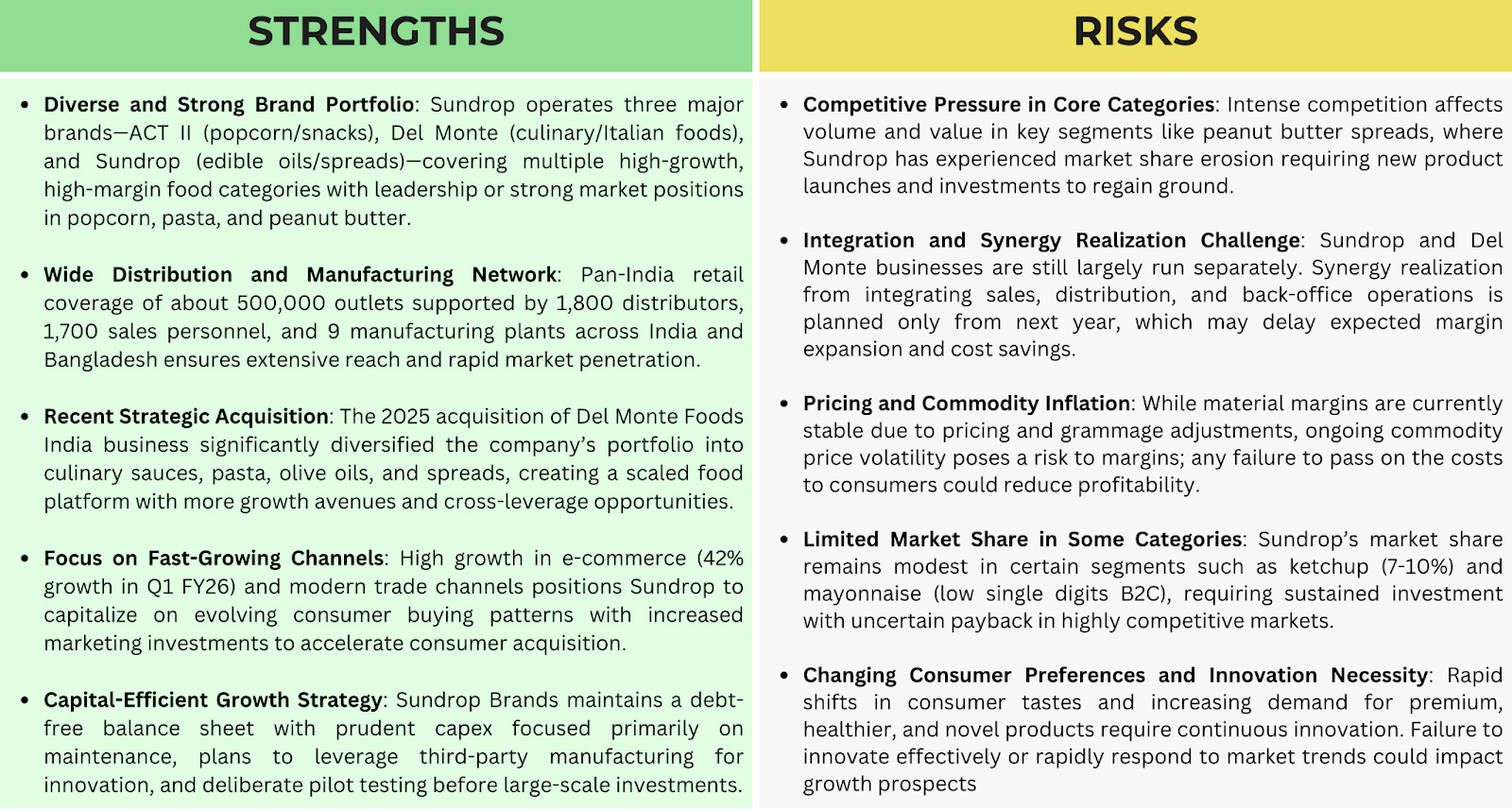

Sundrop Brands’ portfolio is diversified into three main leading brands: ACT II (popcorn and snacks), Del Monte (culinary products including ketchups, sauces, mayonnaise, pasta, olive oil), and Sundrop (edible oils, spreads, breakfast cereals).

Foods segment (including ready-to-eat and ready-to-cook snacks, breakfast cereals, chocolates, spreads) contributed approximately 56% of revenue and grew 15% year-on-year in Q1 FY26.

Culinary segment under Del Monte includes ketchup, sauces, mayonnaise (growing at 8% YoY), and an Italian portfolio (pasta, olive oil, pizza sauces) with volume growth of around 12%.

Edible oils business is stable with volume roughly flat and value growth driven by commodity price inflation.

Peanut butter/spreads segment faces challenges with volume and value declines in traditional trade due to rising competition but has grown 59% in e-commerce.

Del Monte’s channel mix is roughly 40% B2B (food services, key accounts), 50% B2C (modern trade, general trade, e-commerce), and 10% contract manufacturing.

Core categories grew to contribute 61% of revenue in FY26 Q1, up from 59% in FY25, reflecting a strategic focus on these higher-growth, higher-margin segments.

Recent Acquisition and Promoter

In February 2025, Sundrop Brands completed the acquisition of 100% stake in Del Monte Foods Private Limited India business, enabling expansion into culinary and Italian food segments. This acquisition added brands with presence in ketchups, sauces, pasta, olive oil, and more, significantly diversifying the company’s portfolio beyond its original snacking and edible oil base.

The acquisition deal included issuing a 35.4% stake in Sundrop Brands to Bharti Group and Del Monte India Private Limited entities, marking Bharti Group as a significant shareholder with about 21% stake as of March 2025. Other major shareholders include T CAG Tech Mauritius with around 33.9%.

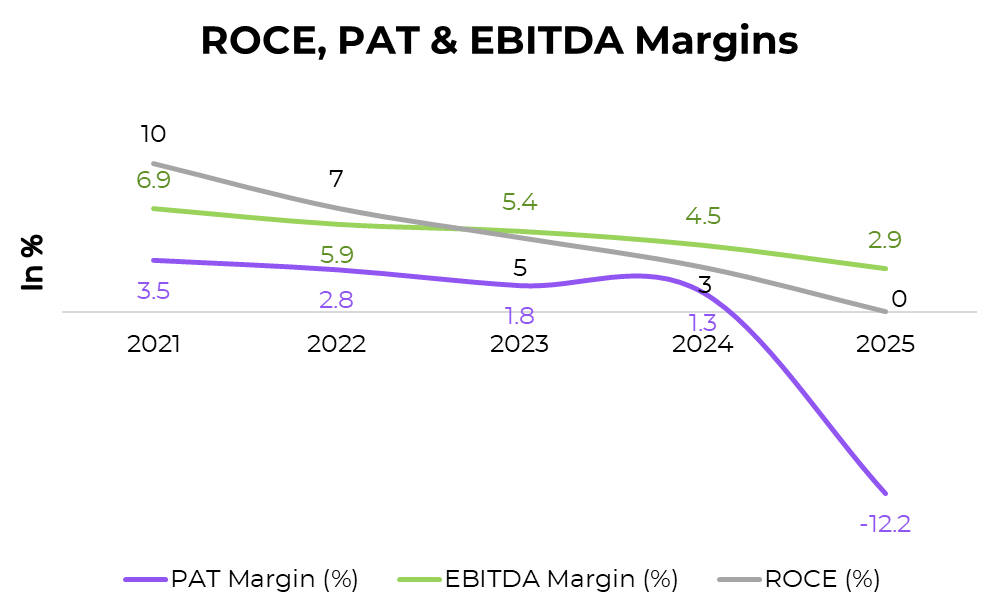

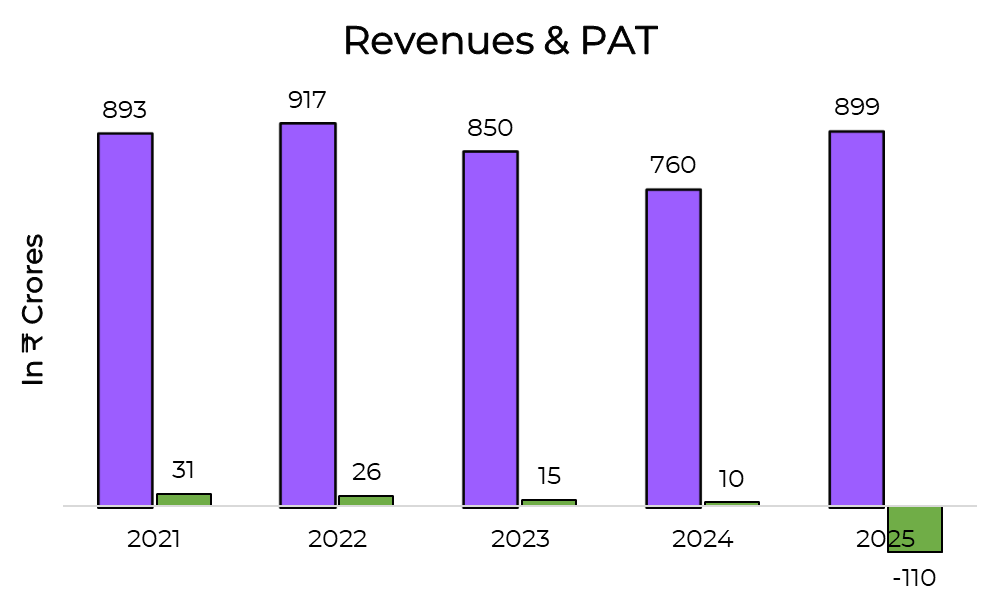

Financials

Why did the PAT dropped ?

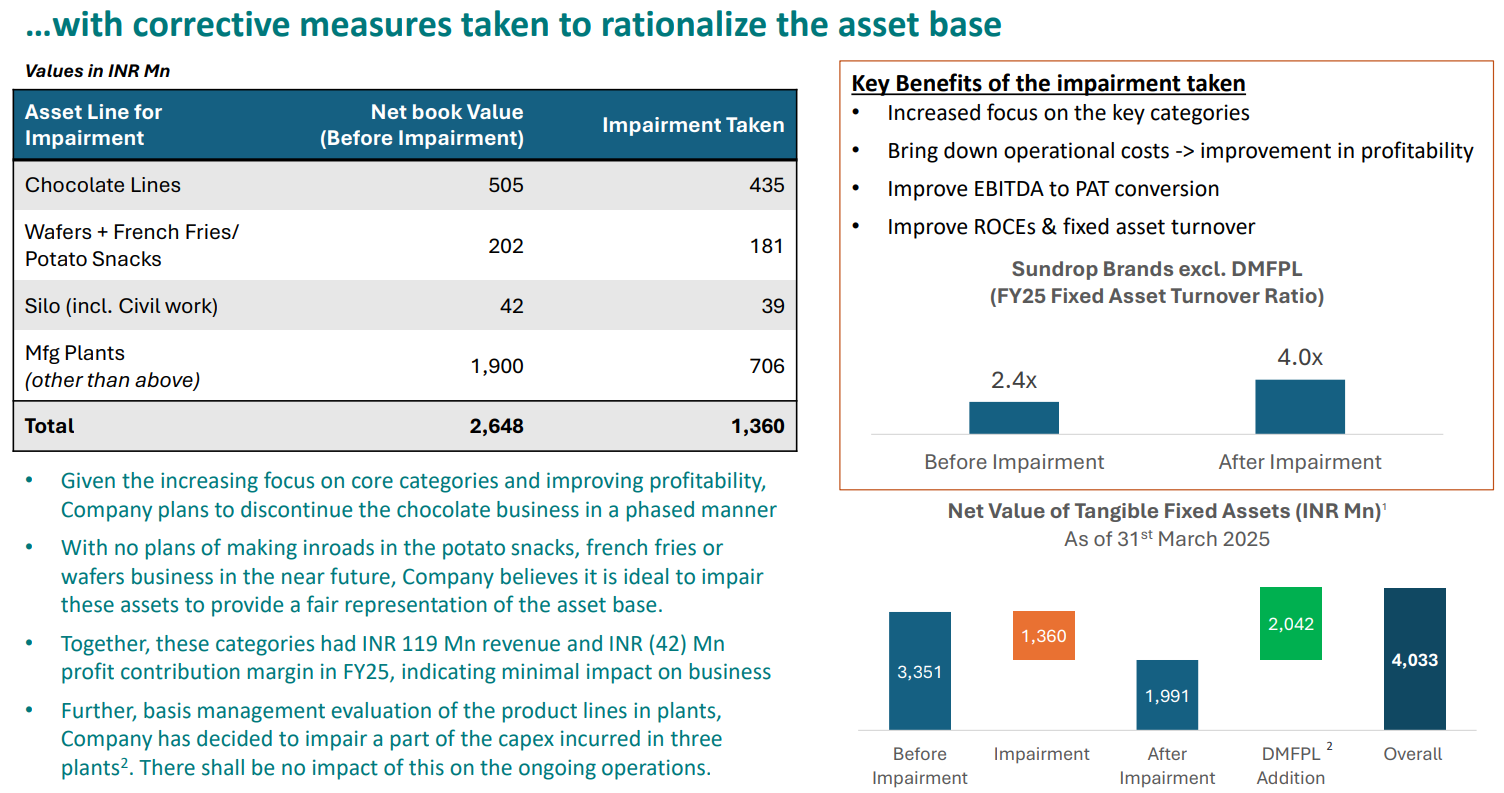

The PAT (Profit After Tax) for Sundrop Brands dropped sharply in FY25 primarily due to significant one-time exceptional expenses that impacted profitability. The most notable factor was the asset impairment charge, where the company wrote down the value of certain non-core manufacturing assets like chocolate, wafers, and potato snack production lines. This impairment was part of their strategy to focus capital and resources on core categories, such as popcorn, culinary, breakfast cereals, pasta, and olive oils, rather than maintaining businesses with minimal contribution or limited future growth prospects.

Additionally, there were added costs related to the acquisition and integration of Del Monte Foods India, including transaction-related expenses, ESOP grants, and advisory charges for business transformation. The reported financials reflect these exceptional expenses, leading to a substantial loss at the PAT level in FY25 even though operational EBITDA showed moderate growth. These impairments and restructuring do not affect ongoing operations but were necessary to present a fair representation of the asset base and improve future capital allocation, fixed asset turnover, and return ratios

Future Outlook

Sundrop Brands is prioritizing a capital-efficient growth approach with the goal of building a significant profitable food platform. Management outlined several key focus areas:

Accelerating growth in core categories such as popcorn, culinary sauces, Italian foods, and breakfast cereals through product innovation, marketing investments, and expanded distribution.

Continuing efforts to regain market share in challenged categories like peanut butter spreads by launching new products and strengthening presence in modern trade and e-commerce.

Leveraging the combined Sundrop and Del Monte distribution networks through pilot projects this year, with plans to integrate operations more closely starting FY27 to realize synergies in costs and marketing efficiencies.

Maintaining operational margin improvements through supply chain efficiencies, procurement optimization, and scale benefits. Normalized EBITDA margin was about 4.4% in Q1 FY26.

Sustaining a debt-free balance sheet and prudent capex focused mainly on maintenance and strategic pilots, with no major expansion capex planned in the near term.

Ambitions remain to grow faster than the packaged foods market (aiming for 4-5% above market) and improve EBITDA margins towards double digits over the medium term through operational leverage, synergy capture, and scale.

The company also plans to rationalize non-core, low-growth businesses such as chocolates and wafers, focusing investments and resources on its core portfolio.

Risk and Strengths

If you an investor who keeps looking for such analysis on small & mid cap stocks, you can join our Emerging Titans model portfolio where we share detailed reports on such ideas. We are SEBI registered Research Analyst (with Registration No. INH000019789)

Disclosure

This article is for educational purposes only and does not constitute investment advice. Readers should consult a SEBI-registered advisor before making investment decisions.

Standard warning

“Investment in securities market are subject to market risks. Read all the related documents carefully before investing.“

Disclaimers

“Registration granted by SEBI, enlistment with RAASB and certification from NISM in no way guarantee performance of the Research Analyst or provide any assurance of returns to investors.”

Superb article, a must read.

Nice Analysis