Skipper Limited — Execution at Record High. The Real Story Has Just Begun.

A ₹9,000 Cr Order Book. A ₹27,000 Cr Pipeline. And a Company Quietly Positioning for Global Leadership.

Welcome to Inside Small & Mid Caps — where we don’t chase price action. We study businesses through concalls, filings, and what management actually says when investors ask hard questions.

Today’s company: Skipper Limited (NSE/BSE: SKIPPER)

Skipper Limited is not a typical industrial company. Established in 1981, it has quietly built a 43-year legacy to become India’s largest and one of the world’s most integrated Transmission & Distribution (T&D) structure manufacturers — covering the full value chain from design engineering and angle rolling, all the way through fabrication, galvanizing, load testing, and EPC line construction.

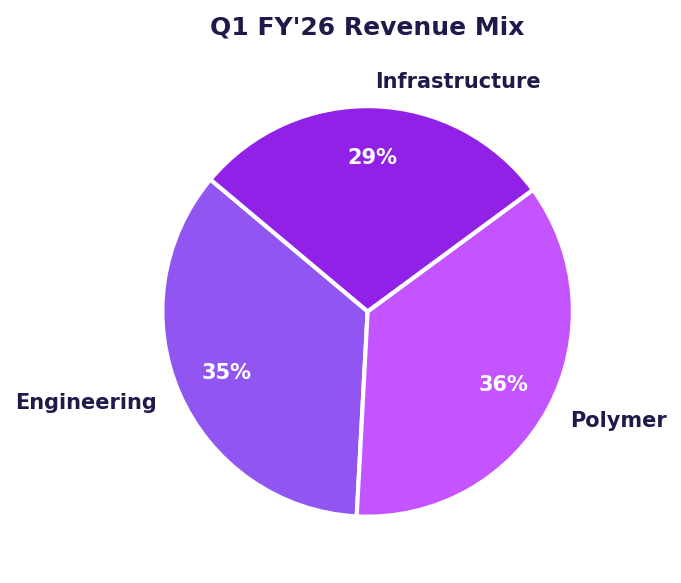

The company operates across three business segments. Engineering — transmission towers, poles, and railway electrification structures — is the crown jewel. Polymer brings high-growth pipes and fittings exposure. And Infrastructure handles EPC execution for transmission line projects. Together, they position Skipper at a rare intersection: deep manufacturing capability + project execution + polymer distribution.

And unlike most industrial manufacturers, Skipper exports to 54+ countries. That’s not an afterthought. That’s a structural differentiation that is now accelerating rapidly.

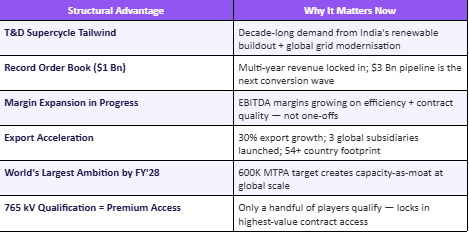

The company has entered what management calls a ‘super cycle of growth’ — catalysed by global energy transition, India’s renewable grid buildout, and a record-breaking order book. Q3 & 9M FY’26 numbers confirm this is not a narrative. It’s happening.

Phase Shift Confirmed — Numbers Don’t Lie

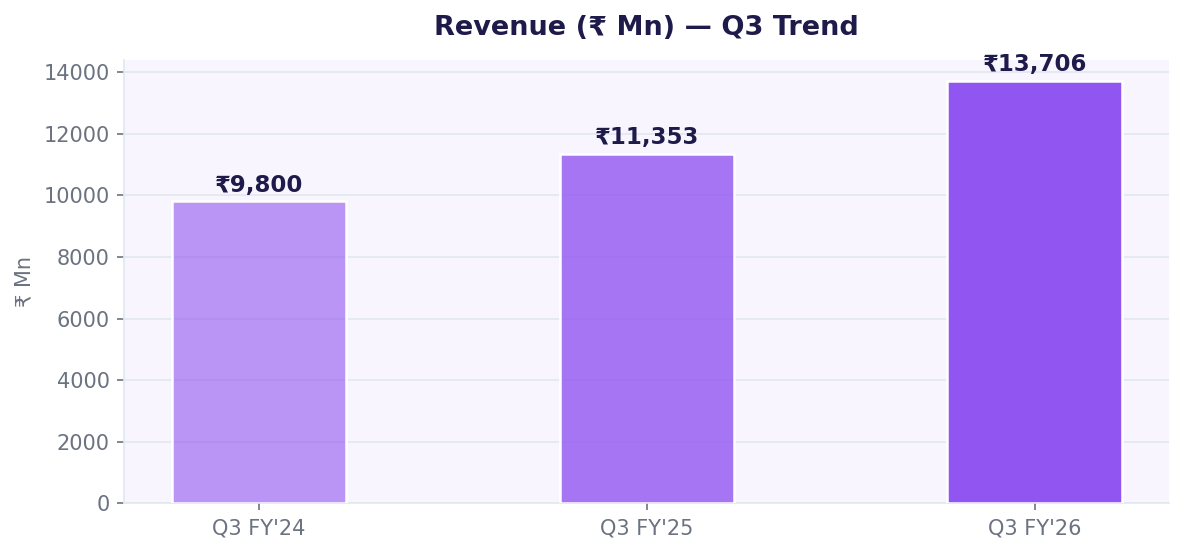

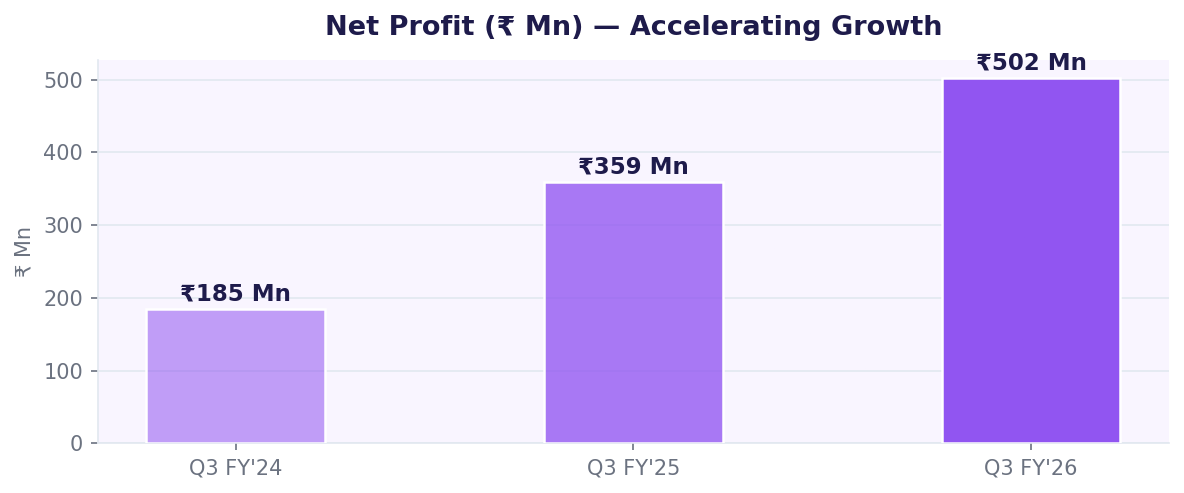

Let’s start with what the latest financials actually show. Q3 FY’26 delivered the highest-ever quarterly revenue, EBITDA, and operating profit for the company. That alone is a milestone. But the compounding across 9 months is what makes this story genuinely interesting

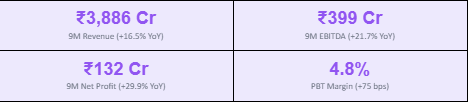

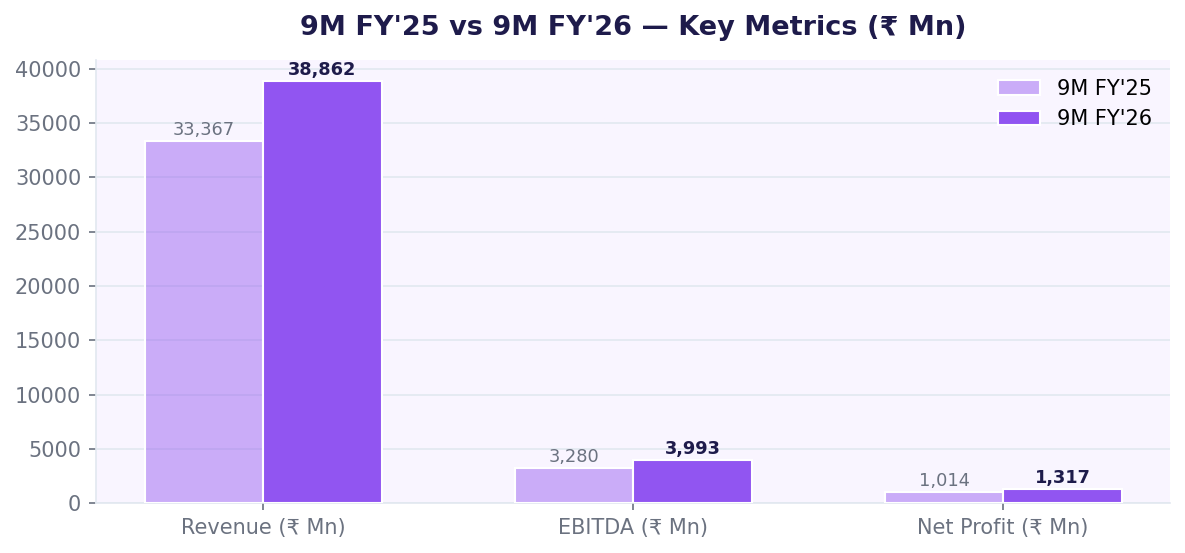

Nine-month performance further confirms the momentum is structural, not seasonal:

Revenue is growing. Margins are expanding. Profits are growing faster than revenue. That combination has a name: operating leverage. And management commentary confirms it’s driven by efficiency and contract quality — not one-off items.

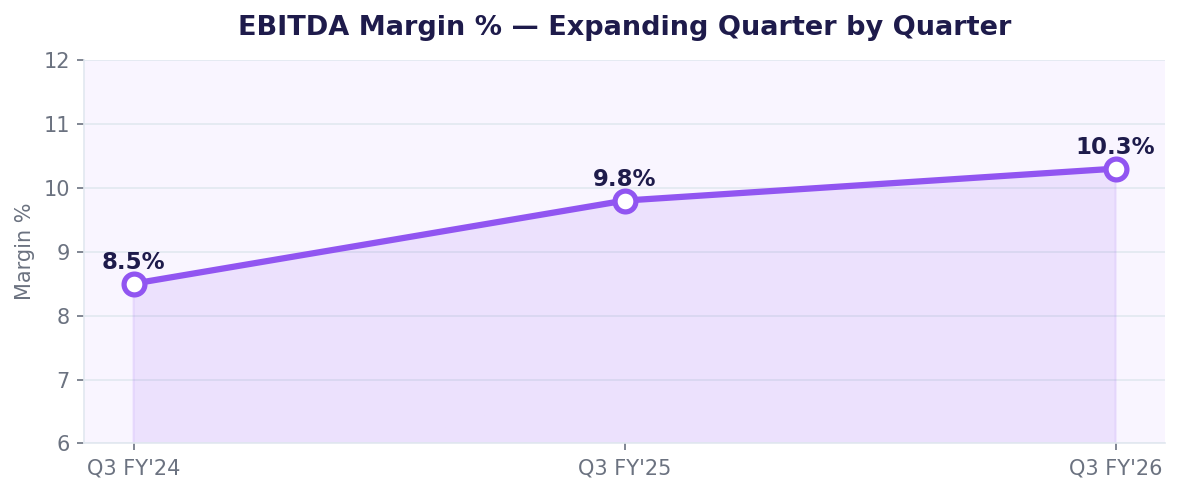

Margin Expansion — Structural, Not Cyclical

EBITDA margins have expanded consistently over the past three quarters, reaching 10.3% in Q3 FY’26 — the highest level in recent history. The Engineering segment alone is delivering 11-12% EBITDA margins and management expects this to sustain. What matters here: management explicitly confirmed that margin improvement came from operational efficiency and higher-quality contract execution — not product mix or one-time items. Efficiency-driven margins are sticky.

Segment by Segment — Where the Growth Is Coming From

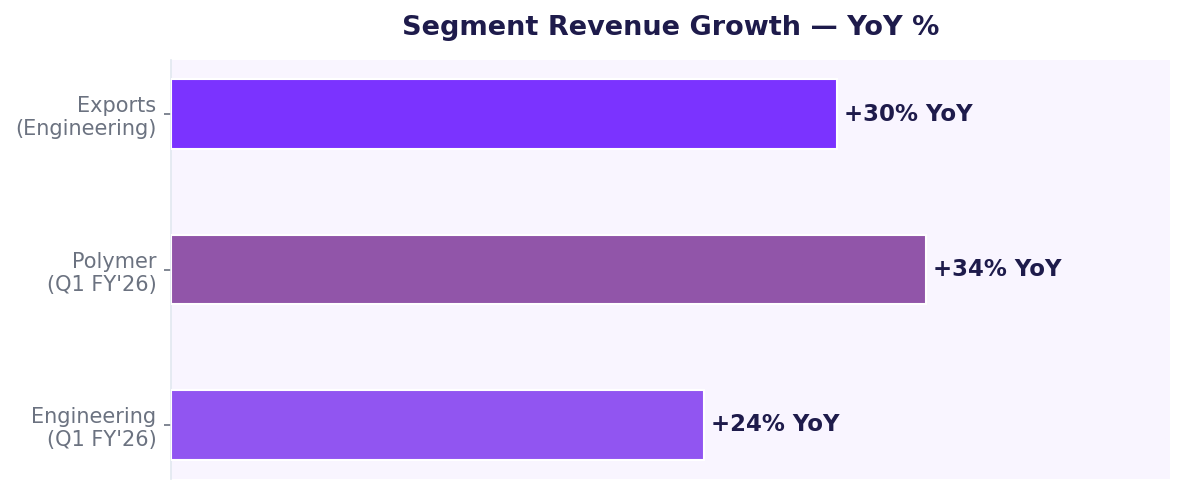

The Engineering segment delivered 24% revenue growth year-on-year in Q1 FY’26. EBITDA margins have now stabilised in the 11–12% range for several consecutive quarters and management is confident this holds going forward.

The Polymer segment surprised on the upside with 34% volume growth year-on-year. The company is actively expanding its retail distribution network — billed distributors grew 39% YoY, and monthly billed retail outlets grew 23%. That’s the foundation of a consumer-facing distribution moat being quietly built.

Exports deserve a headline of their own. Engineering export revenue grew 30% year-on-year to ₹3,254 million in Q1 alone, with exports now accounting for 32% of Engineering revenue. The company has formed subsidiaries in three global regions — Middle East, Latin America, and Asia Pacific — to deepen penetration.

Key export milestone: Skipper secured a major tower testing and design order from the Middle East’s largest utility — reflecting growing global acceptance of its in-house design capabilities.

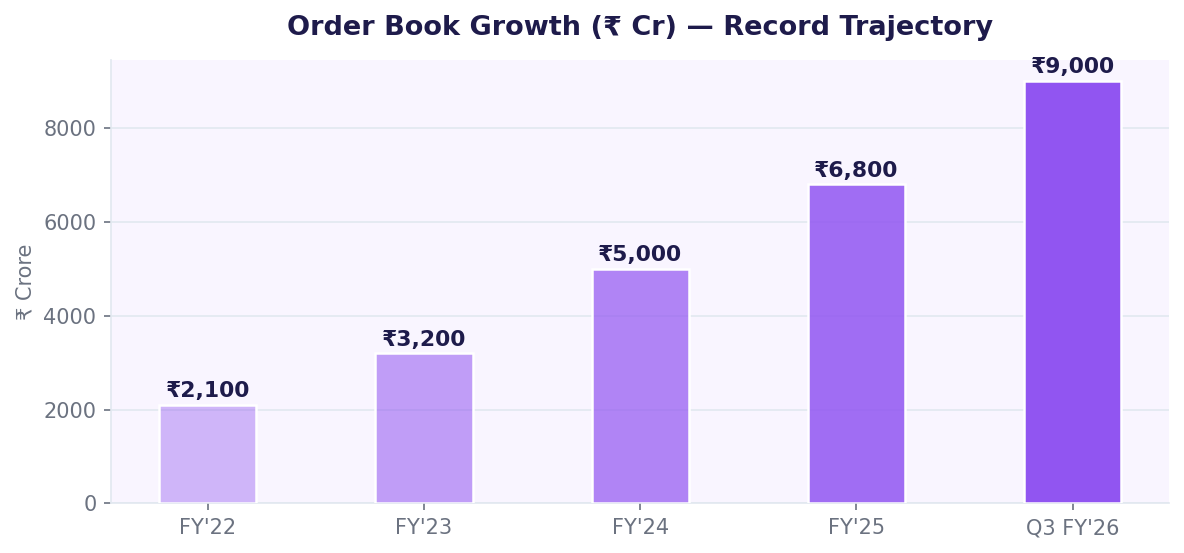

Order Book — An All-Time High With a $3 Billion Shadow

The order book has crossed ₹9,000 crore — approximately $1 billion — an all-time high. But what makes this remarkable is what’s behind it: a bidding pipeline of ₹27,000 crore, approximately $3 billion.

During Q3, the company secured ₹1,429 crore in fresh orders led by Power Grid Corporation and key export markets. In Q1, order inflows surged 158% over the previous year quarter. Skipper secured three prestigious 765 kV transmission line projects from Power Grid in Rajasthan and Andhra Pradesh — its strongest qualification yet in the high-voltage segment.

Order Book Milestone

Pipeline Depth

This is not a thin order book that needs constant replenishment. At current execution rates, it provides genuine multi-year revenue visibility. And the pipeline at 3x the order book means the next round of conversions is when this story really accelerates.

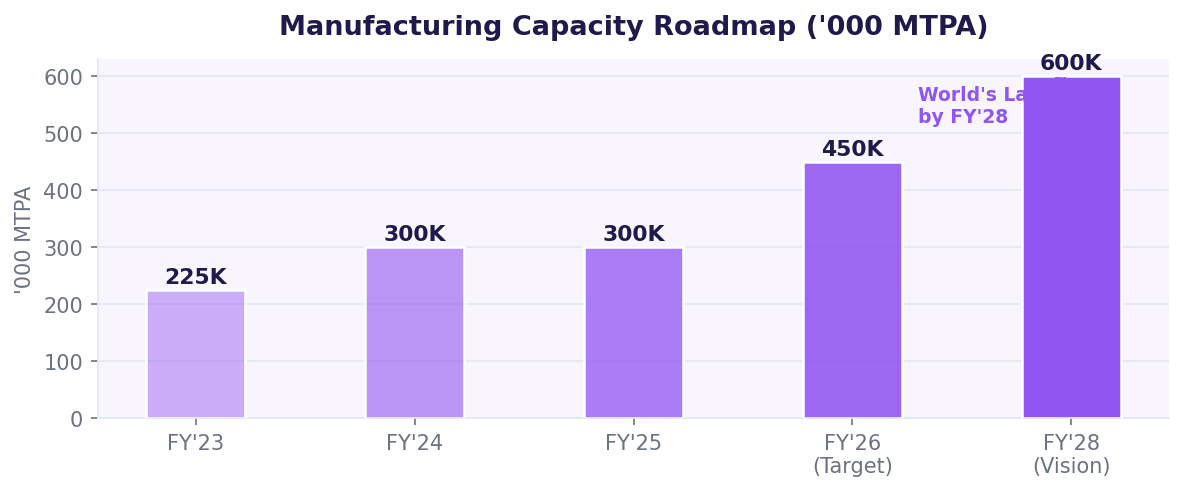

The Capacity Story — Building for a Supercycle

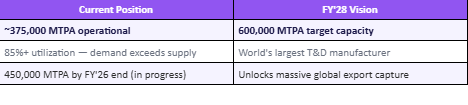

Skipper’s capacity expansion is the under-appreciated part of this story. The company recently commissioned 75,000 MTPA of new capacity — and it’s already fully operational. Capacity utilisation has crossed 85%, meaning demand is pulling on every additional tonne they can produce.

A second 75,000 MTPA expansion is already underway, targeting a total of 450,000 MTPA by the end of FY’26. And management has laid out an even bolder vision: 600,000 MTPA — 6 lakh metric tonnes — by FY’28. That would make Skipper the world’s largest transmission tower manufacturer.

Current Position

FY’28 Vision

New capacity also unlocks fast-track export orders and short-cycle demand — segments where Skipper faced supply constraints last year. The constraint is gone. Now it’s purely an execution story.

The Moat Most Investors Miss — 765 kV Qualification

In T&D manufacturing, not all companies are equal. The ability to execute at 765 kV — the highest voltage level in Indian transmission infrastructure — is a hard qualification gate. Only a handful of companies in India can clear it. Skipper is one of them.

This qualification gives Skipper access to the largest, most complex, and highest-margin contracts in the market. As India pushes toward renewable grid scaling, ultra-high-voltage lines become the backbone of the country’s energy infrastructure. Skipper is already in that ring — and entrenched.

PGCIL awarded Skipper three 765 kV transmission line projects in Rajasthan and Andhra Pradesh in Q3 FY’26 alone — reflecting trust at the highest technical level.

Industry Tailwind — A Multi-Decade Cycle, Not a Quarterly Trade

The context behind Skipper’s growth matters as much as the numbers. India’s renewable energy transition requires massive transmission infrastructure buildout — and that’s not a three-year story. It’s a twenty-year structural shift. Every solar farm, every wind installation, every offshore platform needs transmission infrastructure to carry power to the grid.

Beyond India, the global energy transition is creating demand for T&D structures across markets Skipper already exports to — Middle East, Latin America, Southeast Asia, Africa, and North America. The government’s National Electricity Plan signals policy-backed investment at scale for the long term.

As management put it: Skipper has entered a supercycle. The question is not whether demand will come. It’s whether Skipper can keep up with it.

Digital & Governance — The Quiet Enablers

Two less-discussed milestones deserve mention. First: SAP has gone live. That’s not a headline, but it matters. ERP systems at this scale unlock better production planning, faster order processing, tighter cost controls, and scalability without proportional headcount growth. This is the infrastructure that allows a company to go from ₹4,000 Cr revenue to ₹10,000 Cr without losing operational control.

Second: Skipper has been recognised as a Great Place to Work for the fifth consecutive year. In a capital-intensive manufacturing business competing globally, talent retention is the hidden differentiator between companies that execute and those that don’t.

What Smart Investors Will Track Next

Not the stock price. Watch these execution signals:

Engineering EBITDA margin holding steady at 11–12% across quarters

Capacity reaching 450,000 MTPA by FY’26 end on schedule

Export revenue share crossing 35% of Engineering revenue

Polymer segment sustaining 30%+ volume growth with margin improvement

Order inflow conversion rate from the ₹27,000 Cr bidding pipeline

New subsidiary traction in Middle East, LatAm, and Asia Pacific markets

SAP-driven efficiency gains showing up in working capital cycle improvement

These are the leading indicators that determine whether the current growth trajectory is durable or a peak.

The Bottom Line

Skipper Limited isn’t trying to grow. It’s already growing — at scale, with margin expansion, a record order book, and a capacity roadmap that positions it to become one of the most important T&D infrastructure companies in the world within three years.

Q3 FY’26 didn’t just show a good quarter. It showed a business in the middle of a structural transition — from a strong domestic manufacturer to a globally competitive, export-driven, high-margin industrial platform.

The numbers are speaking. The pipeline is full. The capacity is being built. The question now is not whether Skipper will grow — it’s how fast.

If you an investor who keeps looking for such analysis on small & mid cap stocks, you can join our Emerging Titans model portfolio where we share detailed reports on such ideas. We are SEBI registered Research Analyst (with Registration No. INH000019789

Disclosure

This article is for educational purposes only and does not constitute investment advice. Readers should consult a SEBI-registered advisor before making investment decisions.

Standard warning

“Investment in securities market are subject to market risks. Read all the related documents carefully before investing.“

Disclaimers

“Registration granted by SEBI, enlistment with RAASB and certification from NISM in no way guarantee performance of the Research Analyst or provide any assurance of returns to investors.”