Krishna Defence — Execution Is Rising. The Real Story Has Just Begun

Welcome to Inside Small Caps — where we don’t chase headlines. We study businesses through concalls, filings, and what management actually says when investors ask hard questions.

Today’s company: Krishna Defence & Allied Industries

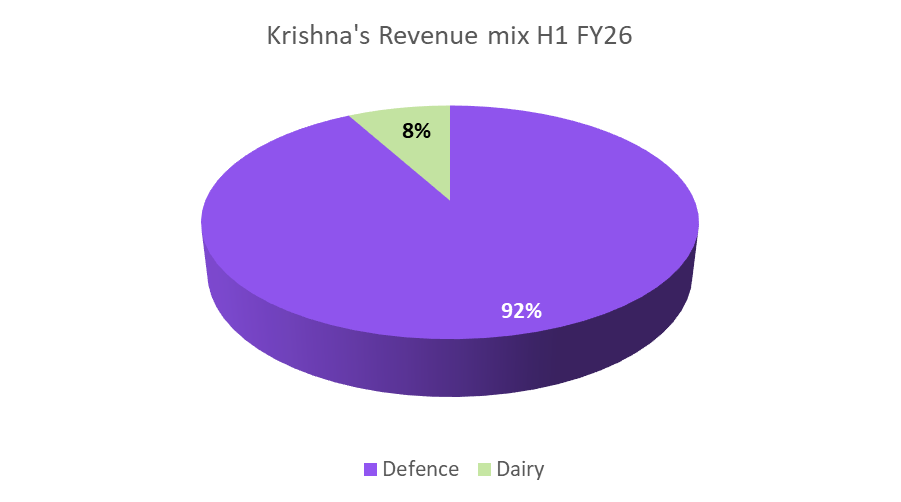

Krishna Defence & Allied Industries is a specialized defence manufacturing company focused primarily on naval systems, high-precision metal components, and critical engineering products used in shipbuilding, underwater platforms, and defence infrastructure. Unlike diversified industrial manufacturers, Krishna operates within tightly qualified segments of the defence ecosystem where supplier approvals are limited, testing cycles are long, and switching vendors is operationally difficult for customers.

The company’s core product portfolio currently includes:

Bulb bars used in naval ship hull construction

Weld consumables for defence-grade fabrication

High-value forged and machined components

Specialized profiles for shipbuilding platforms

Over time, it has been strategically expanding beyond components into higher-value engineered assemblies and structural participation. This reflects a deliberate long-term positioning strategy: move gradually up the defence manufacturing value chain while maintaining capital discipline and operational control.

Krishna’s business model blends in-house manufacturing for mission-critical processes with outsourced non-critical work. This hybrid approach allows the company to scale production without proportionally increasing capital expenditure — a structural advantage that becomes even more powerful when demand accelerates.

Taken together, Krishna Defence today sits at a strategic intersection: niche specialization + expanding capacity + industry tailwinds.

And this is exactly why the latest financial results matter. Because they don’t just show growth.

They show transition.

If you want full historical context on how Krishna Defence created massive wealth for early investors, read our detailed case study here: https://valueeducator.com/sme-stocks/sme-stocks-millionaires-krishna-defence

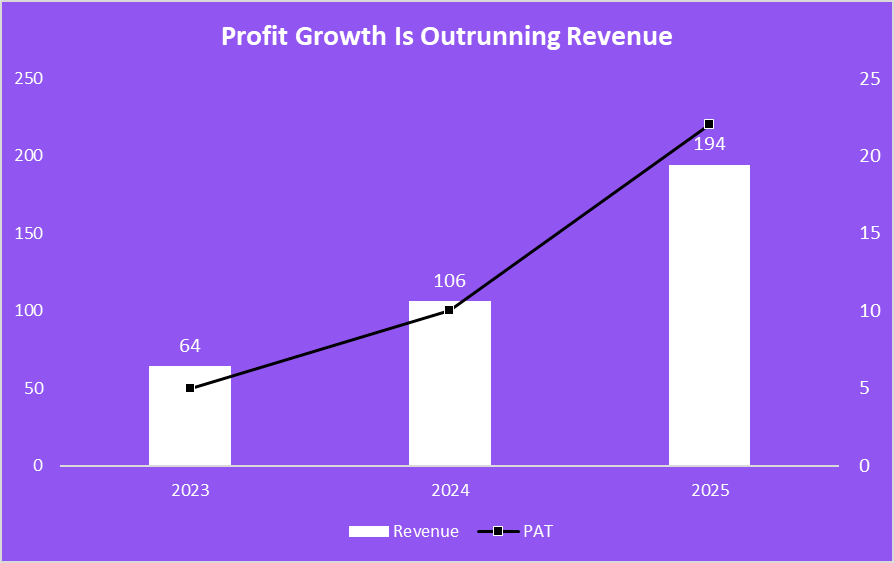

H1 FY26 and Q3 FY26 numbers together confirm that this transition is no longer theoretical — it is already visible in the financials.

Phase Shift Confirmed — H1 Suggested It, Q3 Proved It

H1 FY26 already showed strong operating leverage with revenue growing 28.1% YoY to ₹120.5 crore with:

EBITDA Margins increasing to 17.9% (+291 bps)

Standalone PAT increasing 47.4%, and Consolidated PAT increasing 71%

PAT Margins standing at 15.3% (+383 bps)

This alone hinted structural improvement. But Q3 FY26 confirms it is not temporary.

Q3 FY26 Snapshot — Momentum Continues

Standalone

Revenue: ₹63.7 Cr (+23.4%)

EBITDA Margin: 22.2%

PAT Margin: 16.0%

9M FY26

Revenue: ₹179.9 Cr (+25%)

EBITDA Margin: 20%

Net Profit: ₹25.8 Cr (+77.4%)

The company achieved highest ever Revenue, EBITDA, and Net profit with margin expansion at both EBITDA and Net profit levels.

Investors looking to systematically identify companies showing this kind of scaling behavior can study these early multibagger signals: https://valueeducator.com/multibagger-stocks/early-signals-multibagger-stocks

Revenue is growing steadily, and Profitability is accelerating. That combination usually signals structural operating leverage driven by:

fixed cost absorption

manufacturing efficiency

productivity improvements

And, tighter execution cycles

Management commentary confirms this: margin expansion came from efficiency — not product mix. This distinction matters because Efficiency-driven margins tend to be sustainable.

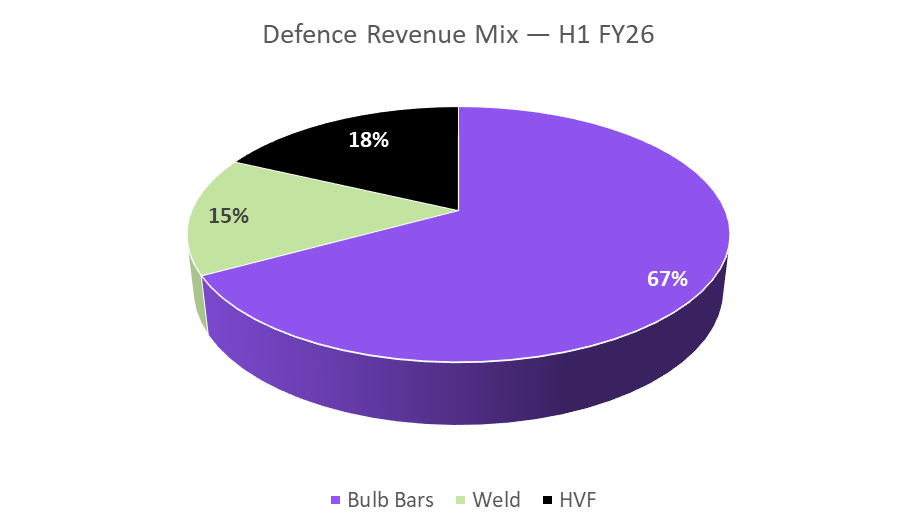

65–70% - Bulb bars

~15% - Weld consumables

~20% - HVF profiles

This reveals a strategic truth:

₹100–110 Cr tenders in pipeline

Expected H2 inflow: ₹100–150 Cr

This is classic defence-sector behaviour: demand visibility precedes order visibility.

Composite naval doors & hatches — trials completed

Large defence castings — import substitution opportunity

Aerospace components — evaluation stage

Advanced weld consumables — development phase

Autonomous Underwater Vehicles (AUVs) — commercialization expected FY27

These are not near-term earnings drivers. They are future margin drivers. Markets consistently undervalue companies in this transition phase.

Structural Milestone — NSE Mainboard Migration

Dec 30, 2025

Frigates

Destroyers

Corvette

LPD ships

Mine vessels

That’s why they maintain confidence in a

India’s coastline expansion to 11,098.81 km (+48%) structurally elevates demand for naval platforms, surveillance systems, and maritime defence infrastructure.

The ₹6.81 trillion FY26 defence allocation (+9.5% YoY) reinforces policy-level commitment toward sustained defence capital spending and platform acquisition.

Taken together, these factors indicate that the sector is not benefiting from a cyclical upswing. It is operating within a

multi-year testing

qualification trials

and certification cycles

Which means:

new platforms mature

AUV programs complete trials

additional products commercialize

shipbuilding demand rises

Capacity expansions stabilize

In other words, the groundwork being laid today starts showing up financially later.

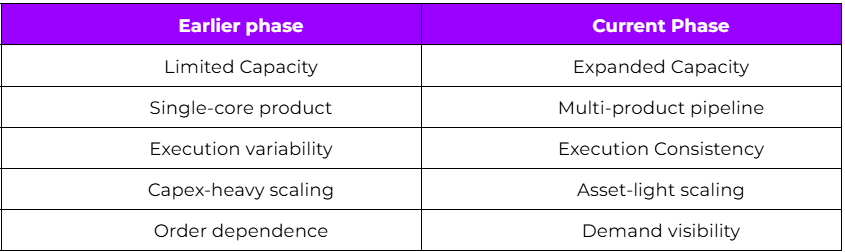

What Q3 Ultimately Establishes

This half-year confirms something important: Krishna Defence is no longer a small supplier trying to grow.

It’s becoming a scaled defence manufacturing platform. Here’s the structural shift:

What Smart Investors Will Track Next

Conversion of H2 tenders

Margin stability near 18%

Autonomous Underwater Vehicle (AUV) trial progress

New product commercialization

Certification approvals

Associate company growth

Because these determine whether growth is durable.

If you an investor who keeps looking for such analysis on small & mid cap stocks, you can join our Emerging Titans model portfolio where we share detailed reports on such ideas. We are SEBI registered Research Analyst (with Registration No. INH000019789

Disclosure

This article is for educational purposes only and does not constitute investment advice. Readers should consult a SEBI-registered advisor before making investment decisions.

Standard warning

“Investment in securities market are subject to market risks. Read all the related documents carefully before investing.“

Disclaimers

“Registration granted by SEBI, enlistment with RAASB and certification from NISM in no way guarantee performance of the Research Analyst or provide any assurance of returns to investors.”

They have given the growth guidance of 30-40% for next few years.

There is an entry to barrier in this business. Let's see how it plays out in future.